Commonwealth Bank of Australia

Genium View.

On all fundamental metrics and using any rational school of thought, CBA is egregiously overvalued. This has been driven by several technical factors in markets and the share registry of CBA rather than any improvement in the underlying business. These factors have been well documented but are largely driven by the investor base being retail focused (meaning fewer sellers), and the shift to passive from the super funds (super funds forced to buy more CBA as its size in the index rises). History shows us that situations like this are not sustainable and at some point CBA will mean revert back to a normal valuation.

The core challenge for shareholders is that there are no clear catalysts on the horizon for CBA shares to fall aggressively and revert to a reasonable valuation in the near term. For this reason, we have avoided telling clients with very large positions to place a full sell, but we instead recommending slowly reallocating to better opportunities elsewhere for future growth.

We do not expect the current valuation to continue to grow higher, so future share price gains will have to be driven by earnings. Earnings growth is muted and will likely come under further pressure as a result of the rate cutting cycle as this places pressure on Net Interest Margins. There are almost no scenarios where CBA's earnings grow quickly enough to justify the valuation, so our base case is that the share price will remain flat for some time to let earnings "catch up" which would in turn seethe valuation multiple fall, rather than the price increasing. The share price could fall if some of the technical factors that have driven the price rise change, some external event shakes confidence in global markets or the Australian banking sector more specifically, but the trigger for this scenario is less obvious at this stage.

Why Fund Managers Dislike the CBA Rally.

Many fund managers are frustrated by the recent rally in CBA’s share price because they’ve been reducing their exposure to the stock over the past 18 months. This has led to under-performance relative to the ASX 200 benchmark. When a small-cap stock delivers outsized returns, it has a limited impact on the index. But CBA is different – its total return of 55%over the past 12 months has significantly outpaced the ASX 200’s 13% gain. With an average index weighting of 10% during that time, not holding CBA meant managers needed to find an additional 3.5% of performance elsewhere just to keep pace – an extremely difficult task.

A Rally Driven by Price-Earnings Expansion.

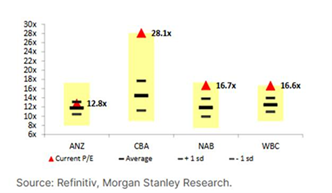

The surge in CBA’s share price hasn’t come from higher profits. Instead, investors are simply paying more for the same level of earnings. CBA’s price-to-earnings (PE) ratio has expanded significantly from its long-term average of 15x, rising alongside the share price from $100 to$191 during 2024–25.

Most of CBA’s earnings come from traditional lending to households and businesses – commoditised products with no brand premium. Despite its extensive advertising, borrowers are generally indifferent between the big banks when it comes to choosing a mortgage provider. In a market with limited credit growth, CBA competes against four other major banks (including Macquarie) offering virtually identical products at similar cost structures.

By comparison, its peers – Westpac, ANZ, and NAB – currently trade on an average PE of 15.5x and yield 4.8%. Yet CBA has surged to become one of the world’s top 10 most valuable banks and the first developed-market bank in history to trade at more than 30x earnings.

Passive Flows Fuel the Momentum.

The real force behind CBA’s rally appears less about fundamentals and more about flows. As the largest constituent in the ASX 200, CBA captures a disproportionate share of money pouring into passive index-tracking funds like iShares, Vanguard and Betashares. This creates a self-reinforcing cycle: rising prices attract more flows, which push prices even higher.

Today, CBA makes up 12% of the ASX 200 – the highest weighting for any single company since News Corp reached 15% during the tech boom of 2000. BHP also hit 15% in early 2009, though that was more a result of holding ground while other large companies collapsed during the depths of the GFC.

CBA’s rise has been remarkable – but it may not be sustainable.

Latest insights

You might also like