Monthly Investment Note - Post Liberation Day

Post Liberation Day – What Happened and What Are The Opportunities?

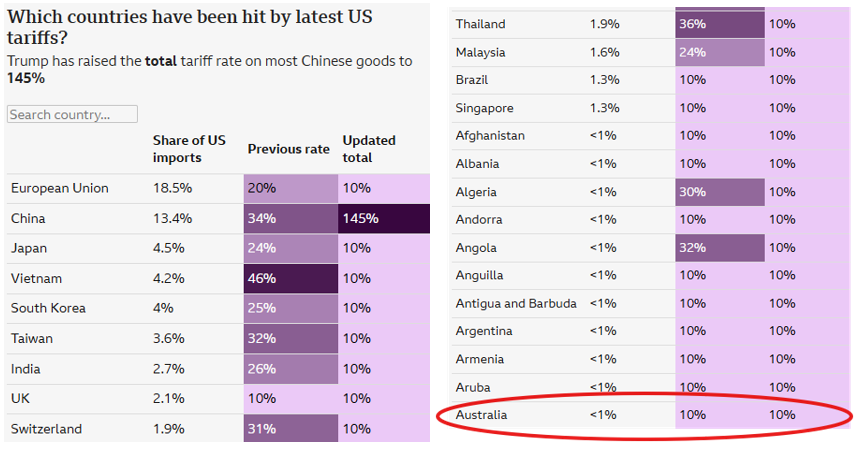

The start of 2025 has been somewhat of a whirlwind ride which peaked on 2 April when U.S. President Donald Trump finally revealed a list of “reciprocal tariff” rates that applied to more than 180 countries and territories. This new chapter in the U. S’s economic history was dubbed Liberation Day. Many started to claim the start of a new trade war however, markets have since bounced back and at the time of writing are at levels above 2 April. In this note we look at the events following liberation day and the opportunities which may present themselves now and in the future.

What happened?

Markets and its participants tend to overreact positive and negative news and on this occasion, the introduction of tariffs by the U.S. was seen as a negative and a significant shift in the powers of world trade. Many have forecast the commencement of a new trade war, increasing the downside risks to growth and upside risk to inflation, meaningful economic slowdowns on a global scale and a general feeling of doom and gloom.

As the world digested the news, global equity markets reacted in kind, falling 10% in the week following the announcement with U.S. markets (the S&P 500) teasing bear market territory, falling approximately 19% since its February highs. A 20% decline officially defines a bear market. This rapid deterioration shocked investors as everything from aerospace parts to toys and video games was to become instantly more expensive for US consumers. Governments began to scramble, companies began to recalculate their expected costs, and the whole world started to look at the global impact of these reciprocal tariffs. What was clearly evident in the immediate days following was the level of uncertainty that had clouded markets. Again, this was evident in the movement of equity market volatility, known in markets as the VIX. It jumped an astonishing 143%, from 21.5 to 52.3. These levels had not been seen since the GFC in 2008, which further emphasised the panic that had engulfed the market.

Changes in market structure over the past 20 years have changed the way markets react to news. These structures are characterised by sharper rallies, deeper corrections, and higher volatility - than in previous decades. This increases stock price momentum, which increases the size of up and down movements in markets. Algorithmic Trading and High-Frequency Trading (HFT) strategies execute trades at extremely high speeds, reacting instantly to market signals also have the potential to amplify short-term volatility. The rise of artificial intelligence could also change how markets operate in the future.

This all leads to more aggressive moves and increased volatility on both negative and positive news. This explains some of the reason for the aggressive fall, and aggressive recovery, that followed the tariffs announcements.

What has happened since 9 April?

It has been a remarkable five weeks since the initial shock. Trump’s “America First” policies, the subsequent sell-off and rising volatility and uncertainty saw countries across the world begin to re-examine their relationship with the U.S and question whether they would continue to be the global steward. More importantly, perhaps it was the kick they needed, governments globally started to plan for a future without a dominant U.S. trading and defence partner and making decisions to get their houses in order to ultimately become more stable. Outside of reacting with tariffs of their own, many countries took countermeasures to protect their own interests and to shore up confidence amongst its people. China and the European Union, namely Germany are planning to introduce significant stimulus packages to boost growth at least in the near term, several other countries have announced government emergency packages to support those industries most at risk whilst those with limited room to manoeuvre have entered into negotiations with the U.S. in order to trash out a better deal.

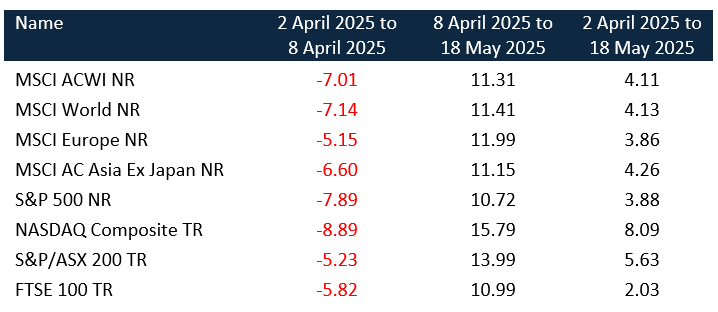

As all this was taking place, Trump unveiled a stunning reversal on tariffs, pausing most country-specific tariffs (by 90-days) but at the same time, ramping up duties on China imports. This sparked a market rally that has ultimately led markets to their pre-liberation day levels. The S&P 500 lost 8% in the first week, 2 April to 8 April, post liberation day, but has since returned 10.7% (8 April to 18 May) and is up 3.9% since the announcement. The ASX 200 fell 5.2% in the first week but has since returned 14% and is up 5.6% since the announcement. See table below major market movements.

Was this a case of markets getting it wrong? Was it a further example of market resilience and appreciating the fact that plenty of other opportunities exist outside the U.S.? Or was it always the strategic ploy by President Trump, risking global recession and immense backlash, to rattle the cages of countries he thought were not pulling their weight to potentially lower tariffs and non-tariff barriers?

Whatever the reason for the rally, be it the rollback of tariffs, trade negotiations or a shift in sentiment, major indices have not only recovered their losses form that fatal week but have reached close to their highs of February. Volatility has also fallen quite significantly however uncertainty will remain elevated at least for the next 90 days.

What are the opportunities?

We see this as a great opportunity. Perhaps the shock the world needed to realise the golden opportunities non-U.S.equities, in this instance, hold. Could this, for example, be the start a of European renaissance? Investors had become obsessed and over-invested in the U.S.off the back of the ‘Magnificent 7’ and the valuation gap with other markets had gone way too far. Europe generated much better-than-expected earnings in Q4 2024 and the economic prospects for Germany have notably improved and are on the up. Momentum driven markets over the past two years is slowly abating and fundamentals are beginning to once again be the drivers of company performance. This further opens the door for the under-valued European markets which have experienced numerous headwinds since the GFC. As noted above, the EU is loosening the purse strings, particularly in Germany, to fund infrastructure/transportation, energy and housing. This is a meaningful shift in attitude and should stoke employment and GDP.

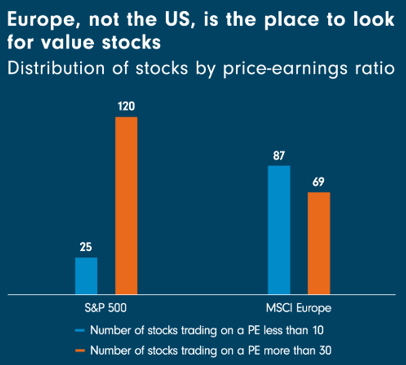

European stocks remain attractively priced, supported by strong fundamentals and growth potential, presenting undervalued investment opportunities. European stocks have started the year trading at significant discounts compared to U.S. equities. Even after these recent gains, the forward price-to-earnings ratio for European stocks remains well below that of its American peers, offering a compelling value proposition for investors seeking alternatives to the high valuations in the U.S. market.

Sector tailwinds are also providing valuation support. European and U.K. banking sectors are offering pockets of opportunity whilst German utilities including energy companies have upside potential given the massive infrastructure plan recently announced and improving investor sentiment. Sectors however exposed to exports-such as automotive,and pharmaceuticals have experienced increased volatility and downward pressure on stock prices following tariff announcements. However, these have not been harsh as previous market shocks and with the U.S not imposing new direct tariffs on Europe, it has allowed European equity markets to remain in a fairly positive state. In general, European markets are also more diversified across banks, commodities, and industrial, which are currently benefiting from the macro environment. This is in stark contrast to the U.S. market which is dominated by the technology sector. This of course provides are far more diversified opportunity set and after years of under-performance, investors have and continue to be underweight European equities, meaning even modest inflows can have a pronounced effect on prices.

Europe aside, compelling arguments can also be made for the relative under-performing global emerging markets regions of Asia and in particular, Latin America. Valuations gaps relative to large cap U.S. equities and developed nations in general, has persisted for quite some time. Emerging markets account for approximately 10-15% of global markets and with central banks in these regions having far more flexibility in regard to monetary policy, companies which are able to cut costs and/or find new markets, can be expected to undergo positive re-rating. Importantly, emerging market growth is underpinned by favourable demographics, urbanisation, and a rapidly expanding middle class, leading to higher consumption and investment opportunities.

Outside of equity markets, real assets and private markets such as infrastructure, real estate, private equity, etc. also offer attractive opportunities. As we enter a new phase of opportunity in 2025 and beyond and with long-term strategic themes such as digitisation, deglobalisation, energy transition and the every changing geopolitical landscape, sectors and strategies that are aligned with long-term structural trends and resilience will become more important.

Rather than doom and gloom, perhaps Liberation Day can be seen as a trigger for opportunity rather than a deterrent. As with any market shock, uncertainty and volatility will dominate markets in the short and medium-terms however it could prove rather fruitful in the long-run as new and dormant markets attract new capital plus provide valuation and diversification benefits.

What could tariffs mean for your portfolio?

Although equity markets have recovered from the post-Liberation Day sell-off - primarily due to the rollback and delay of tariffs and the progress in trade negotiations - the post-Liberation Day environment for global equities can possibly be seen as the commencement of a new paradigm in global trade and international investing. Although initially characterised by heightened uncertainty and volatility, the need for a more selective and considered approach could be paramount for future success. While risks are elevated, especially from trade disruptions and policy unpredictability, there are also opportunities arising from sector rotation, regional divergence, and attractive valuations outside the U.S. Diversification, adaptability and risk management will be key for investors navigating this potentially new era.

To discuss the impact of the above information on your portfolio, please speak with your adviser.

Latest insights

You might also like