Market Weakness on US Economic Concerns

Market Update.

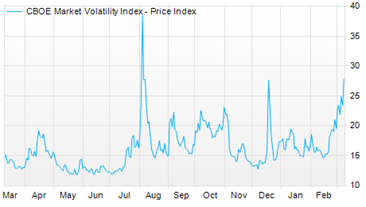

The US equity market has now fallen more than 8% over the last month, and 5.05% calendar year to date. In addition, US government bond yields have fallen sharply (prices higher) whilst a widely used measure of equity market volatility is almost 70% in the last month.

Closer to home, the ASX 200 is down over 8% in the past month, following the US markets lead.

These moves are in stark contrast to the month of January and much of 2023 and 2024 where equity market movements were incredibly strong.

What's changed?

Investors have become unsettled given US policy uncertainty, particularly relating to tariffs, and recent comments from both the US Treasury Secretary Scott Bessent and US President Donald Trump who haven’t ruled out a US recession in the short term.

This backdrop is challenging the market’s rather entrenched soft-landing narrative which was previously hoped for and largely delivered in 2024 but may be short-lived.

What are the key items to note?

Whilst tariffs were well telegraphed and expected in 2025, the lack of certainty regarding who they apply to (allies vs adversaries), when they apply (delays and adjustments), and who or what will be exempted from tariffs has made investors nervous whilst also creating uncertainty at the household and business level in terms of their current and future spending and investment. Tariffs are complicated to understand, particularly without a lens to longer term history, but many of those announced do seem to be transactional in nature (i.e. used for negotiating purposes).

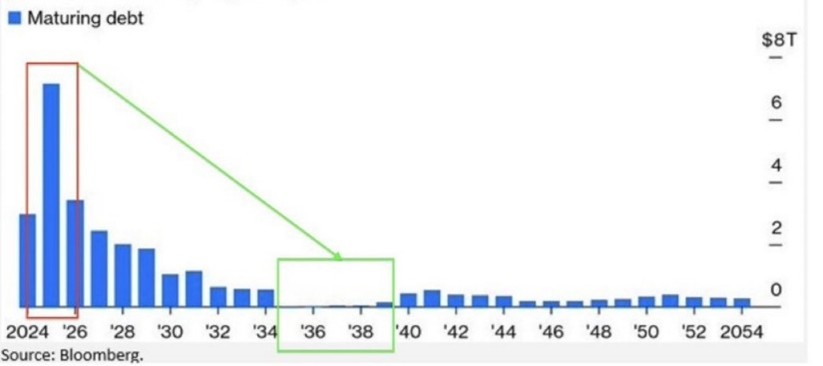

US debt levels have also been a focus given the US Treasury has an arduous task to refinance plenty of expiring debt this year and would obviously like to do so at the cheapest borrowing rates possible. Whilst historically that would be handled via applying significant political pressure on the US central bank to lower the cash rate, that can’t and won’t be done in the current cycle given underling inflationary pressures. That means the US Treasury and the Trump administration need to get craftier when it comes to getting bond yields lower. That craftiness may lead to some rather unorthodoxy policies which is unnerving investors currently.

US employment has been the bastion of hope behind the soft-landing mantra of the last couple of years. However, signs of cracks are starting to appear. Recent jobs growth data has been weaker than expected with downwards revisions to previously released data. In addition, job cuts are now at their highest level since the GFC, whilst the composition of US jobs growth shifts aggressively away from the public sector to the private sector. This shift can involve some lag which may result in weaker consumption at the household level.

Why is this happening?

The new Trump administration was given a clear mandate by the US people at the 2024 election. This mandate is centred on change and significant change at that, effectively focused on cleaning house so that the US exerts its power (soft and hard) globally from a healthy home. This includes securing the border, ensuring a more fairer playing field on trade, and repairing a severely damaged budget filled with graft so they can begin to deliver on primary election promises including tax cuts and deregulation.

The problem with signing up for this sort of significant change is you inevitably need to go through some pain in order to course-correct. Whilst the Trump administration is arguably off to one of the most transparent starts in US history, three unanswered questions remain:

- How much pain can the US economy handle in the very short term as it transitions?

- When will they come out better for it out the other side?

- As this transpires, what does this mean for broader investment markets?

What does it mean for your portfolio?

Whilst US and Australian equity markets have fallen more recently, particularly US technology names, European, UK, and emerging markets have fared better calendar year to date. This shows that investor discipline might be returning and is a good reminder that valuations do matter even though it’s been a long time between drinks. Notably, the US and Australian equity markets traded at elevated levels through much of 2024 and even as recently as January this year.

Bonds have held up well in the short term, particularly those at the more conservative end of the spectrum (i.e. government bonds and high quality investment grade credit).

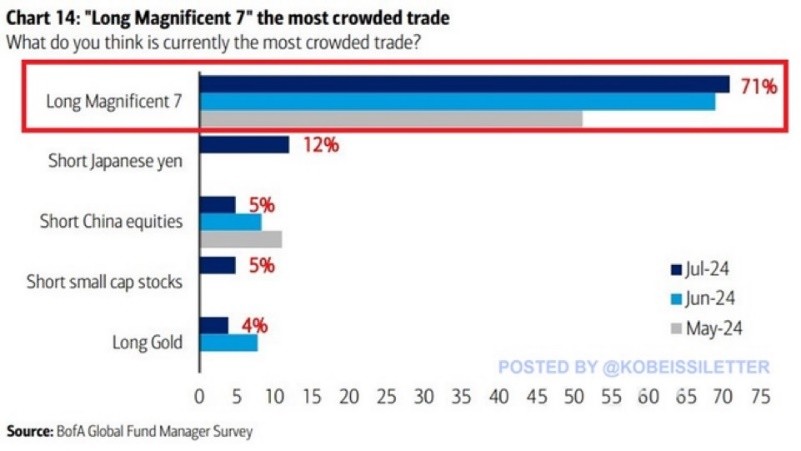

This is an environment where diversification (rather than concentration) and a cautious (rather than performance-led) stance really matter as crowded trades come under pressure and really test momentum-led investor resolve.

What should I do?

Whilst the actions being taken by the Trump administration may be unnerving, they are certainly not surprising. All were well telegraphed ahead of time and have been explained at length on an almost daily basis since January 20.

We see the current weakness in some asset prices as somewhat justified given we felt expectations leading into 2025 were too lofty to begin with. The heat is coming out of more expensive parts of the market and rotating into more under-owned parts of the market, which is healthy.

It’s key not to get caught up in short term noise and messaging from traditional news sources, which generally does a good job of inciting fear and further panic. Portfolios under our purview are generally well diversified and already adopt a rather cautious stance. This means we can remain focused on the longer term whilst standing ready to take advantage of opportunities as they arise, particularly when panic sets in.

For now, remain watchful and careful in your approach to investing, but there’s no immediate need for panic.

Latest insights

You might also like